There was rampant speculation after the Federal Open Market Committee (FOMC) meeting last week about the timing and number of interest rate cuts this year. In a follow-up interview on 60 Minutes on Sunday, Federal Reserve Chairman Jerome Powell did not sound like someone who has pivoted.

In fact, Powell believes the Fed can wait until it sees more labor damage before cutting the Federal Funds Rate aggressively or moving toward a neutral policy stance, saying again that a March rate cut is “unlikely.”

In December, the Fed talked about three rate cuts in 2024 but some people made a case for four, five or even six rate cuts given a Fed pivot. However, for me it’s always been about the labor market and jobless claims data, and that data line hasn’t broken enough for the Fed to be more aggressive. For the Fed to cut rates in March, we would need weaker labor data, no matter how low inflation goes in the next report.

Here’s part of the interview on 60 Minutes that illustrates what I’m talking about:

Scott Pelley: But inflation has been falling steadily for 11 months. You’ve avoided a recession. Why not cut the rates now?

Jerome Powell: Well, we have a strong economy. Growth is going on at a solid pace, the labor market is strong, 3.7% unemployment. With the economy strong like that, we feel like we can approach the question of when to begin to reduce interest rates carefully. We want to see more evidence that inflation is moving sustainably down to 2%. We have some confidence in that, our confidence is rising. We just want some more confidence before we take that very important step of beginning to cut interest rates.

Notice the statement, “We feel like we can approach the question of when to begin to reduce interest rates carefully.” This is the old and slow part I have been discussing since the end of 2022. The Fed already has a restrictive policy and if the labor market was breaking today they would be cutting rates aggressively. However, instead of getting ahead of the curve and getting out of restrictive territory into neutral policy, they will take their time on this and stay restrictive for a bit longer.

This has been a theme of my work since 2022 and is why I favor labor data over inflation data at this stage. Back in 2022, the Fed discussed having the Fed Funds rate mirror three, six and 12-month PCE data. Today, PCE three-month and six-month inflation is running below 2%, headline 12-month PCE is running at 2.6%, core PCE 12-month is running at 2.9% and the Fed funds rate is over 5%.

With that kind of improvement in inflation, why is the Fed risking being restrictive with its policy? It’s because they will feel better about cutting rates when the labor market is breaking. The data line that will change everything is not more BLS jobs Friday reports like we just had, but the jobless claims data. It is simply too low for the Fed to pivot.

We are going to see rate cuts this year. The Fed believed that policy was too restrictive when the 10-year was near 5% and we had 8% mortgage rates, but they seem fine with mortgage rates between 6%-7.25% right now. Here’s another quote from the 60 Minutes interview:

Pelley: The next meeting around this table that will decide the direction of interest rates is in this coming March. Knowing what you know now, is a rate cut more likely or less likely at that time?

Powell: So, the broader situation is that the economy is strong, the labor market is strong, and inflation is coming down. And my colleagues and I are trying to pick the right point at which to begin to dial back our restrictive policy stance.

This clearly shows that the Fed hasn’t pivoted now, they just didn’t want their policy to be too restrictive. The last thing they want on their plate is a job-loss recession going into an election year after they hiked so high so fast.

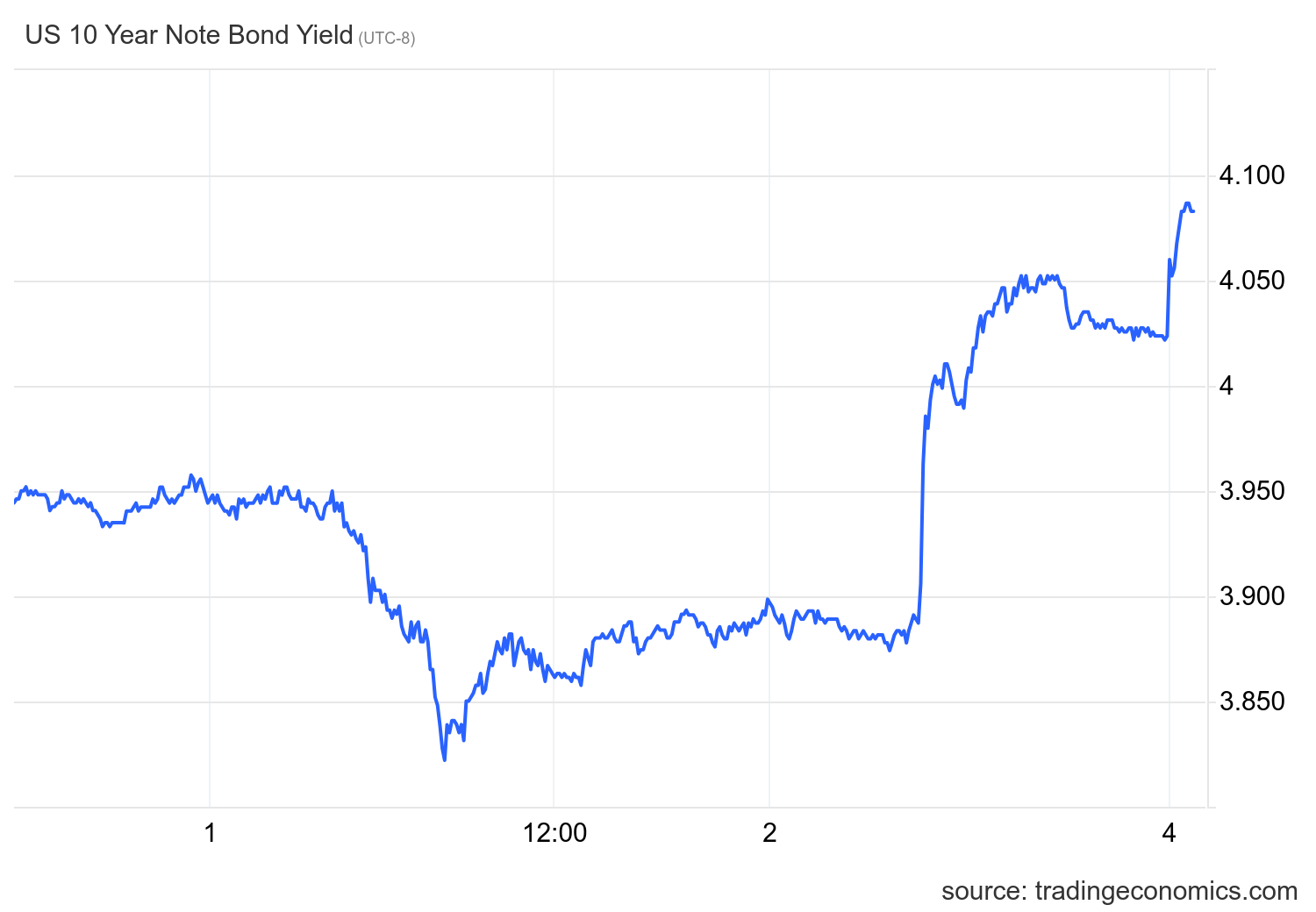

Let’s take a first glance at the bond market reaction to the interview. The 10-year yield headed higher after this interview went live, rising from 4.02% to 4.07%.

The 10-year yield is the key for housing in 2024. In my 2024 forecast, I set the 10-year yield range between 3.21%-4.25%, with a critical line in the sand at 3.37%. If the economic data stays firm, we shouldn’t break below 3.21%, but if the labor data gets weaker, that line in the sand — which I call the Gandalf line, as in “you shall not pass” — will be tested.

This 10-year yield range means mortgage rates between 5.75%-7.25%, but this assumes spreads are still bad. The spreads have been improving this year so much that if we hit 4.25% on the 10-year yield, we won’t see 7.25% in mortgage rates.

Below is the chart of the 10-year yield since Feb. 1 and you can see the reaction after Powell talked on 60 minutes Sunday: yields went higher.

We are in the upper-end range of my 10-year yield forecast, and jobless claims are near the historical bottom of the post-COVID-19 recovery. My model is based more on claims data, so this looks about right.

Powell didn’t discuss housing at all in this interview and the Fed is in a kind of no-man’s land when talking about housing. The only silver lining I can say here for the housing market is that if the Fed didn’t talk about a 5% 10-year yield and 8% mortgage rates being too restrictive with Fed policy. We might be there today after the last jobs report! That’s the most positive spin I can take from the recent actions — that they know they were pushing the limits with the housing market.

Remember, most recessions start with losing residential construction jobs so they’re mindful of this reality in an election year.

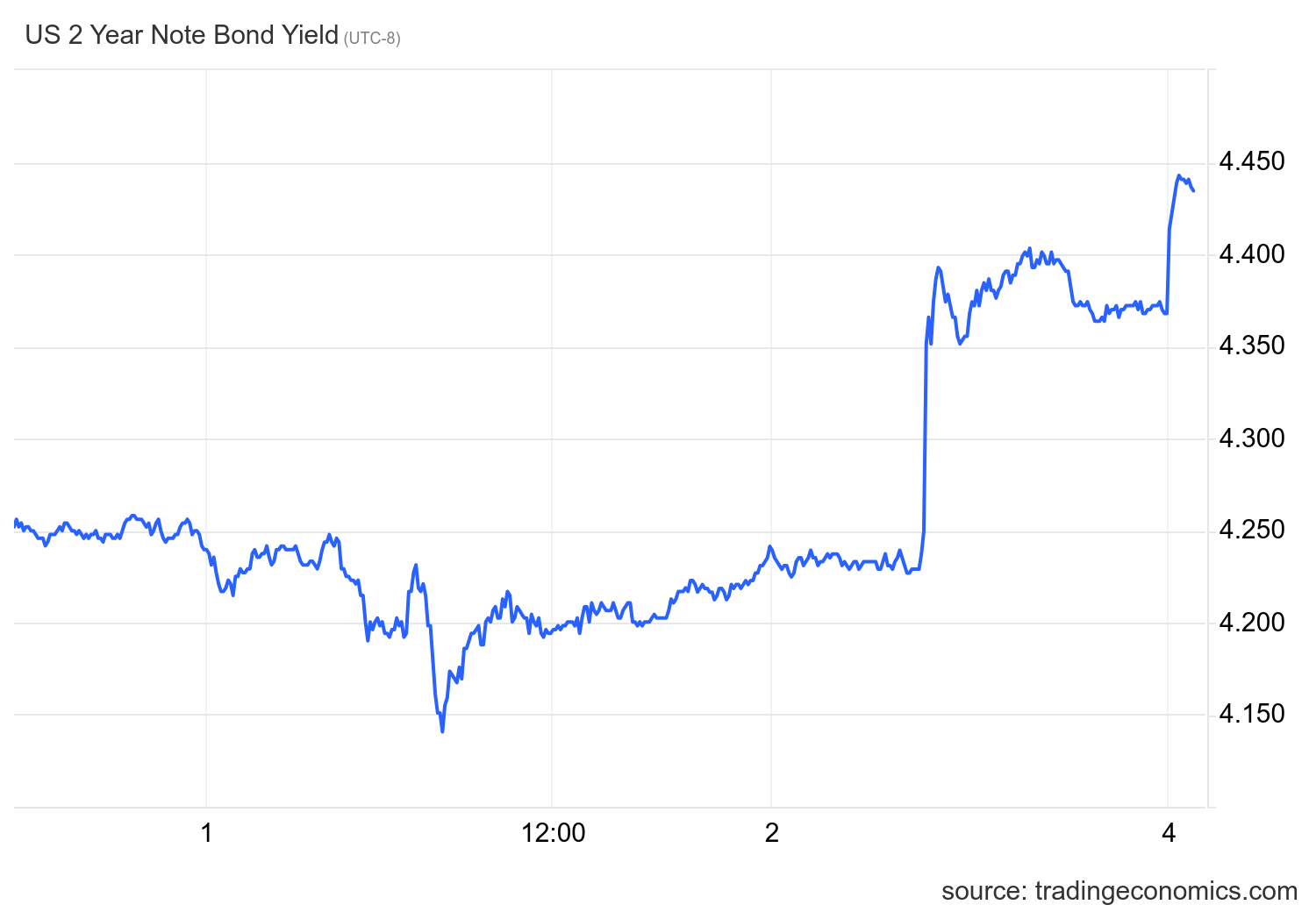

At this point of the cycle, if you want an idea on rate cuts, the 2-year yield is the best place to go. I will stand firm on getting no more than three rate cuts in 2024 unless jobless claims get to 323,000 on a four-week moving average. Unfortunately, if the Fed hasn’t pivoted by then it will be too late. Right now, the 2-year yield is rising from recent lows, making more aggressive rate cut forecasts unlikely.

Like the 10-year, the chart of the 2-year yield below shows a strong reaction to the 60 Minutes interview.

Powell’s latest interview makes it clear: Nothing big will change over the next few months no matter what happens with inflation — the labor market hasn’t broken enough for the Federal Reserve to pivot.